AI-driven document authentication to prevent claims fraud

This case study highlights how insurers may be able to counter increasingly sophisticated claims fraud using AI‑powered document authentication, informed by our partnership with Fortiro in Australia.

Loading ...

Background

Insurers and customers want swift resolutions when a claim is filed, and technology is pushing straight-through processing and automation to new levels. However, in the quest for greater speed, anomalies in documents submitted may be missed when reviewing claims. This issue is compounded as fraudsters are becoming more adept at exploiting the vulnerabilities of digitisation and finding new ways to make false claims. Claims are increasingly in digital formats and fraud is becoming harder to spot. Indeed, some fraud is mostly invisible to the human eye due to digital document alterations.

So, if digital technology and document automation are both a business strength and a weakness, how can insurers maximise the benefits of digitalisation while reducing the risks?

Description of solution

To address this, Hannover Life Re of Australasia Ltd partnered with a leading fintech that combines security with speed when assessing the authenticity of financial documents. Fortiro began as part of a consulting firm in Australia before being spun off to form a separate company. The Fortiro Protect platform provides a ‘forensic view’ of financial documents. It draws on a blend of technologies that scan and analyse content in documents. This includes artificial intelligence, optical character recognition, detailed image analysis, and natural language processing. Collectively, when harnessed for a specific task, for example, in this case to authenticate financial details, these technologies help resolve claims quickly while enhancing security.

Documents are assessed across a wide range of fraud indicators including areas such as strange fonts, spelling mistakes, unusual layouts and digital alteration. The software typically runs more than 100 fraud checks in less than one minute by analysing document layout, content and digital construction. By using AI-based rules, claims assessors can profile everything from the way a document looks to the terminology that is used, right through to the metadata and a document’s digital history.

Results

The Fortiro technology was already proving its worth in the banking sector, primarily for high-volume credit card and mortgage sales. Hannover Life Re of Australasia Ltd wanted to test its potential in the insurance world. To do this, we ran a successful proof-of-concept trial with direct life insurance claims where we tested the system on claims where fraud was known and claims where fraud was suspected.

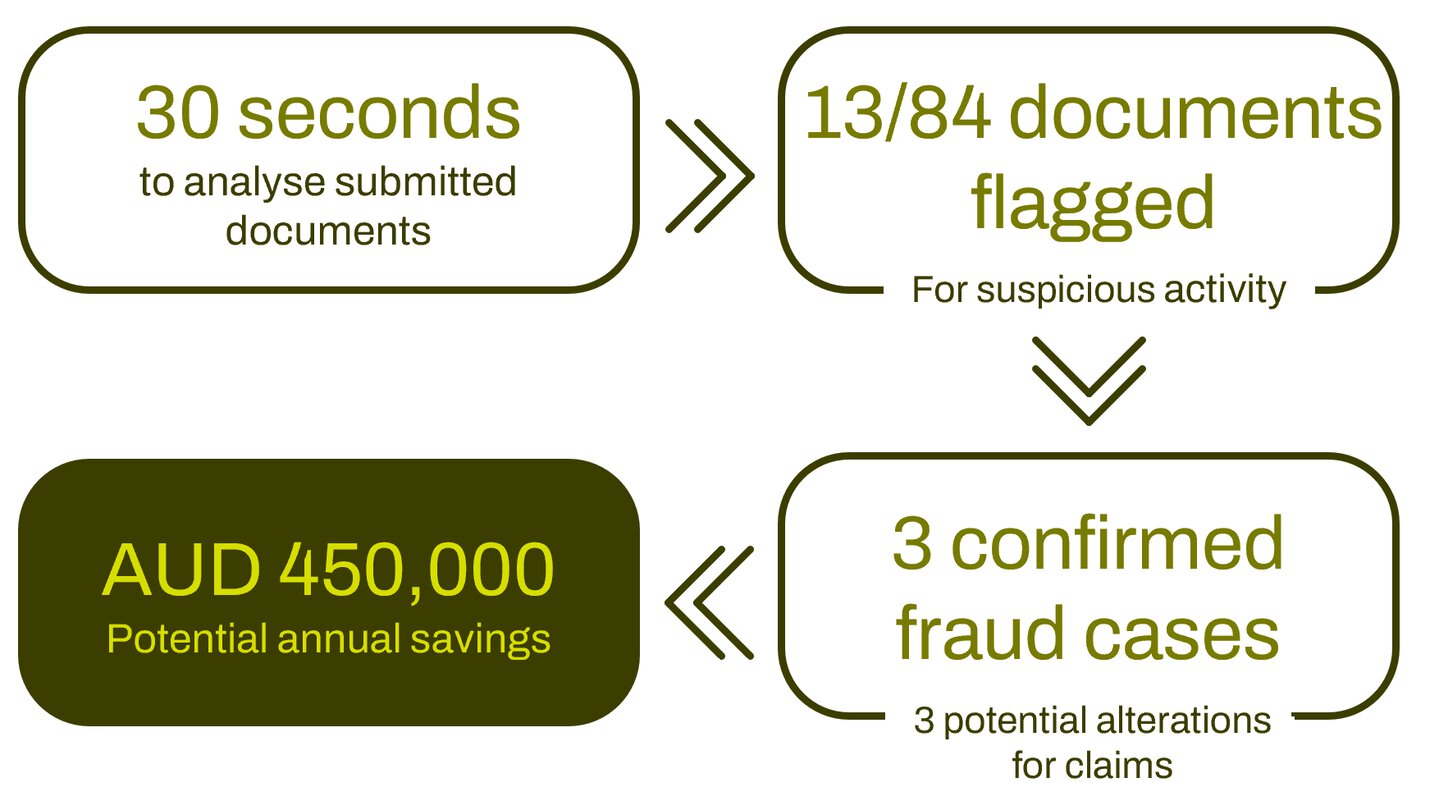

A proof of concept was designed to test using Fortiro's technology on 84 historical claims documents. These documents were categorised into three groups: those with previously detected fraud, suspected but unproven fraud, and genuine claims. The results were remarkable: within just 30 seconds, Fortiro's technology identified suspicious flags in 13 documents, leading to the confirmation of three instances of fraud and potential alterations for three more claims. This translated to a potential annual saving of AUD 450,000, showcasing the efficiency and effectiveness of Fortiro's fraud detection technology.

Fortiro key results

The results of this pilot look very promising for life insurance. The results revealed strong potential to reduce claims leakage where the technology had confirmed total permanent disability (TPD) and income protection (IP) claims fraud or highlighted probable fraud needing further investigation before a payout can be approved.

Because Hannover Re is a direct insurer in Australia as well as a reinsurer, we have now progressed beyond the pilot to implement the technology in our own insurance business. At the same time, on the reinsurance side, we are spreading the word and promoting the benefits for carriers in the local Australia market.

Having already demonstrated that the platform can be used to identify financial income fraud, we are staying at the forefront of the use of this technology in insurance by pursuing additional use cases. We have been working with Fortiro to extend the functionality to Australian Death Certificates, another document type that has a high fraud risk and often high sums insured. A further potential area is to assess medical documents. Doctors’ reports, blood tests, death certificates, and other medical submissions could all benefit from this AI-enhanced analysis.

.png)

"The technology flagged all the known fraud cases and identified why the suspicious ones were fraudulent. Moreover, it also spotted fraud where this hadn’t been suspected.”

Implementation & process considerations

Beyond Australia, for insurers looking to implement fraud detection solutions, we believe it’s important to work with credible partners at the cutting edge of identifying fraud.

Carrying out a proof-of-concept pilot on the historic book of claims can be a suitable first step to assess the value that the software will deliver. This requires suitable data to be maintained to run the pilot. Where value is proven through fraud detection and process efficiency gains, the solution can then progress to the live implementation phase.

Post implementation, it is important to monitor the value being delivered on an ongoing basis, and to ensure your fraud detection partners continue to stay one step ahead in deploying the latest technology for fraud detection.

How Hannover Re can support you

Hannover Re has a structured assessment process to support you to validate partners and a proven track record on delivering innovations in partnership with tech providers and our insurance partners. We would be delighted to work with you to jointly source, pilot and scale fraud detection solutions in your market.

Disclaimer:

The information presented in this case study, as well as in any other descriptions of projects or cooperations, is for general informational purposes only and does not constitute legal advice, regulatory guidance, medical advice, or any form of professional advisory service. To avoid any wording that could be interpreted as implying medical effectiveness, this document must not be understood as containing, asserting, or suggesting any medical efficacy claims. Nothing in this document shall be construed as a legally binding offer to enter into any contract or agreement of any kind. All results, performance indicators, and outcome descriptions reflect the specific conditions and parameters of the referenced project(s) or product launch(es). They are not guarantees, promises, or assurances of comparable or future performance in any other context. No warranty is given – whether express or implied – particularly that comparable or similar results can or will be achieved elsewhere. Any potential success of comparable initiatives critically depends on the lawful and compliant ability to contact policyholders, including the validity of any required consent under the applicable legal framework. All third‑party entities mentioned in this document, including insurtech companies, are independent businesses and operate separately and autonomously from Hannover Re. Their services, solutions, or technologies are neither endorsed nor guaranteed by Hannover Re and are subject to their own terms and conditions, unless explicitly stated otherwise. References to third‑party trademarks or brands are made solely for descriptive purposes and remain the property of their respective owners. No affiliation, sponsorship, approval, or endorsement by those owners is implied. Statements in this document regarding benefits, compliance requirements, risks, risk assessments, or business cases are based on our subjective experience, judgment, or interpretation. They do not replace - and must not be relied upon as a substitute for - independent assessment, verification, or due‑diligence activities by customers or other stakeholders. In particular, all aspects relating to data protection requirements (including but not limited to GDPR considerations) and AI‑related regulatory obligations must be independently assessed, verified, and evaluated by interested parties in light of their own legal and operational frameworks. The use of the terms such as “partner” or “partnered” without further qualification solely indicates that we cooperated on specific activities or exchanges with third parties; it does not imply a legal partnership, joint venture, affiliation, or any form of shared corporate structure. Each party acts independently and on its own behalf. Hannover Re and/or affiliated companies of the Hannover Re Group assume no liability for the accuracy, completeness, or future applicability of the information provided in this document.