.png)

AI video technology for health and risk insights

This case study highlights the value of AI video selfies for life and health underwriting, drawing on insights from our pilot in South Africa.

Loading ...

Background

As digital health solutions rapidly evolve, insurers are exploring innovative ways to assess risk and engage customers. AI-powered video selfies, utilising Transdermal Optical Imaging (TOI) technology, offer a novel solution by analysing facial geometry and blood flow to estimate health metrics like BMI, blood pressure, and heart rate variability.

This pilot explored the value of integrating video selfie technology into the life and health insurance application process, focusing on two areas:

Customer appeal:

Evaluating the overall appeal, user experience and engagement with Nuralogix’s Anura app across diverse customer cohorts.

Accuracy:

Comparing Anura’s health insights with clinical data collected nurses during standard underwriting assessments, focusing on BMI, blood pressure, blood glucose, and cholesterol.

Over 26 weeks, 1,650 insurance applicants and staff from two South African insurers participated in the study to compare Anura’s video selfie health insights with traditional medical screenings.

.png)

Description of solution

Anura’s AI-powered video selfie uses geometric and blood flow analysis from a 30-second video selfie face scan. This can be readily captured from a smartphone or computer camera. Based on this face scan, the technology predicts a range of health and wellness metrics such as heart rate, heart rate variability, body mass index (BMI), breathing rate, blood pressure, cholesterol risk, and diabetes risk (HbA1c).

Biometric signals from the face, assessed using TOI, are uploaded to Nuralogix’s cloud, where they’re processed into health insights. No photos or videos are stored or shared, instead only the derived health signals are returned to the insurer, providing insights into the customer’s wellbeing.

Results

Customer adoption and appeal

In total, 1,650 people completed an Anura video selfie: 1,379 insurance customers and 271 staff.

Among eligible participants, 50% opted in, despite the video selfie not reducing application time due to parallel medical testing being done to validate accuracy. Adoption is expected to increase if the technology improves and streamlines the process by reducing medical tests.

Participation skewed toward individuals under age 40, indicating strong appeal among younger demographics who are potentially open to discover health-related insights in a non-invasive way, and could be particularly valuable for insurers looking to attract business from customers in these segments.

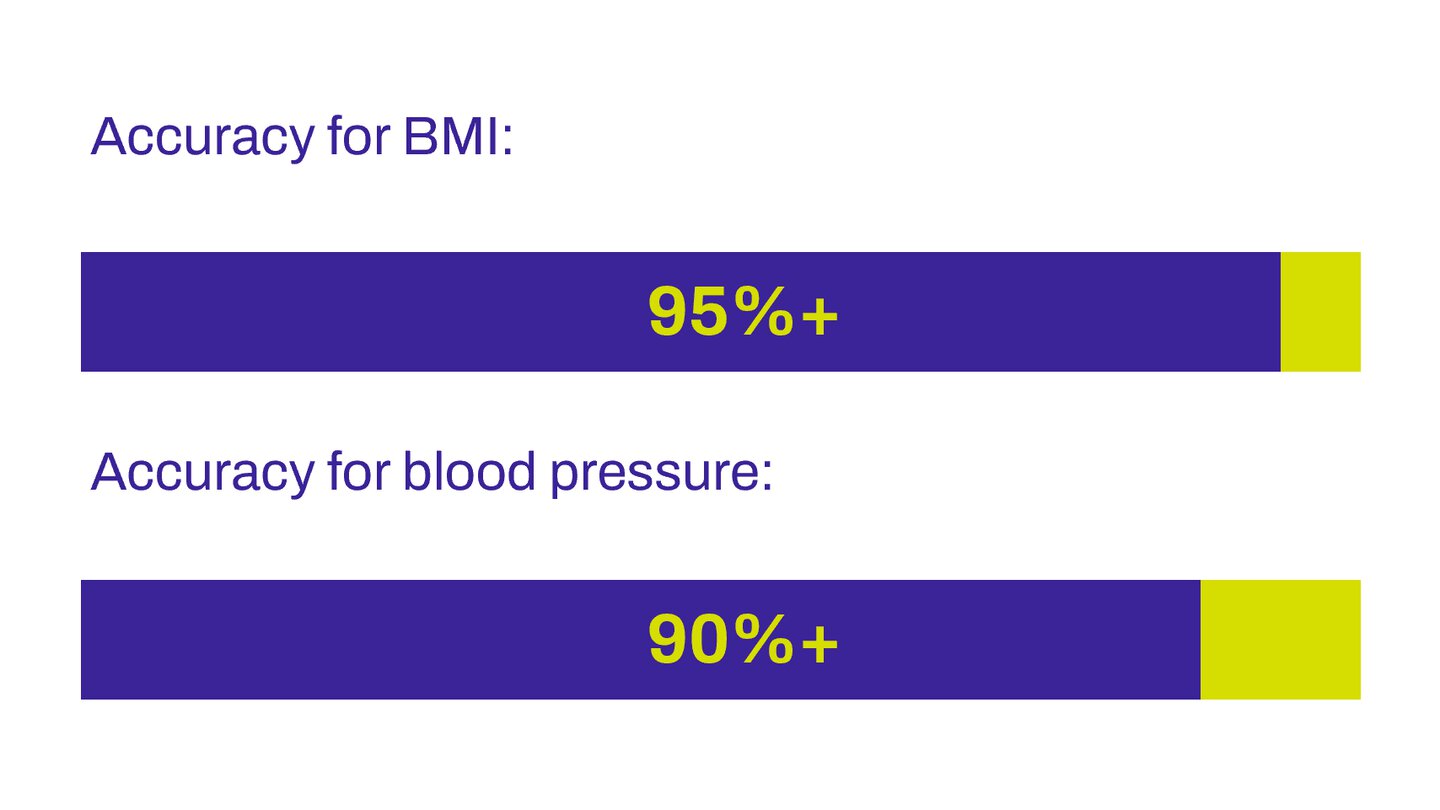

Pilot results on real-world accuracy of the technology

The technology showed high accuracy for BMI (95%+) and blood pressure (90%+). However, there were more type 2 errors where video selfies incorrectly predicted low blood pressure despite actual readings being normal. This raises concerns about using video selfies as a substitute for traditional medical underwriting, as it could miss high-risk individuals during screening. Additionally, this may lead to anti-selection by high-risk applicants, weakening an insurer’s risk pool quality.

Real-world accuracy of Anura's technology

Predictions for HbA1c and cholesterol were less reliable but expected to improve with further development.

Accuracy was consistent across age, sex, and race, supporting equitable use. Overall, the pilot highlights strong potential for video selfies in insurance globally, especially with continued refinement and integration.

BMI is a key indicator used in the assessment of health risk so to have the technology producing such high accuracy is very encouraging, not just for its use now, but also for the potential of other measures to increase in accuracy over time.”

Conclusions from the pilot

The pilot highlights the potential of AI-powered video selfies to deliver health insights across the life and health insurance value chain. Continued customer education is essential to building customer adoption and trust in such new health technologies.

Distribution and compliance:

- Attract younger customers: The technology could be used to attract younger, - individuals to the insurer. This is driven by the finding that this technology appeals to under-40s who are keen to discover insights about their health in a non-invasive way.

- Support lead prioritisation: Accurate predictions for BMI and blood pressure can help to screen applicants, enabling insurers and agents to prioritise leads. To protect the risk pool and avoid anti-selection, these applicants should still undergo traditional underwriting to validate health status, making video selfies a complementary tool, not a replacement.

It is also important to keep in mind that data protection (privacy) and laws and AI regulations define strict requirements with regards to “automated decision making” in general and in L&H insurance distribution in particular. Assessing the applicable legal requirements is crucial in this area.

Underwriting:

- Reduce BMI non-disclosure: Video selfies can help detect misreported BMI, a common issue in self-reported data. Research suggests that more than 1 in 5 customers with a weight considered as unhealthy may misrepresent their weight when self-reporting BMI at point of underwriting. Including this step may also deter misrepresentation through a sentinel effect.

- Improve risk classification for limited underwriting products: For products with no or limited medical underwriting, video selfies can be used as a supplement to enhance risk classification. This additional information can allow for more risk-adjusted pricing, thereby enabling business growth for the insurer.

In-force and claims:

- Beyond the pilot, video selfies could support ongoing customer health awareness with enhanced engagement and wellbeing with potentially lower claims costs. Regular access to health insights may help customers monitor changes and manage risks.

- For example, some participants reported that the pilot flagged elevated HbA1c or cholesterol, prompting them to seek medical follow-up in the traditional healthcare setting. This shows how regular access to health insights can identify risks earlier, helping customers manage changes and potentially reducing claims, benefiting both the customer and insurer.

How Hannover Re can support you

With the pilot showing the value that AI-powered video selfies can provide, Hannover Re is keen to support insurance carriers worldwide to embed this technology into their L&H insurance products and processes.

We are happy to share further insights on this pilot, and partner with you to explore opportunities to improve underwriting and other insurance processes.

Disclaimer:

The information presented in this case study, as well as in any other descriptions of projects or cooperations, is for general informational purposes only and does not constitute legal advice, regulatory guidance, medical advice, or any form of professional advisory service. To avoid any wording that could be interpreted as implying medical effectiveness, this document must not be understood as containing, asserting, or suggesting any medical efficacy claims. Nothing in this document shall be construed as a legally binding offer to enter into any contract or agreement of any kind. All results, performance indicators, and outcome descriptions reflect the specific conditions and parameters of the referenced project(s) or product launch(es). They are not guarantees, promises, or assurances of comparable or future performance in any other context. No warranty is given – whether express or implied – particularly that comparable or similar results can or will be achieved elsewhere. Any potential success of comparable initiatives critically depends on the lawful and compliant ability to contact policyholders, including the validity of any required consent under the applicable legal framework. All third‑party entities mentioned in this document, including insurtech companies, are independent businesses and operate separately and autonomously from Hannover Re. Their services, solutions, or technologies are neither endorsed nor guaranteed by Hannover Re and are subject to their own terms and conditions, unless explicitly stated otherwise. References to third‑party trademarks or brands are made solely for descriptive purposes and remain the property of their respective owners. No affiliation, sponsorship, approval, or endorsement by those owners is implied. Statements in this document regarding benefits, compliance requirements, risks, risk assessments, or business cases are based on our subjective experience, judgment, or interpretation. They do not replace - and must not be relied upon as a substitute for - independent assessment, verification, or due‑diligence activities by customers or other stakeholders. In particular, all aspects relating to data protection requirements (including but not limited to GDPR considerations) and AI‑related regulatory obligations must be independently assessed, verified, and evaluated by interested parties in light of their own legal and operational frameworks. The use of the terms such as “partner” or “partnered” without further qualification solely indicates that we cooperated on specific activities or exchanges with third parties; it does not imply a legal partnership, joint venture, affiliation, or any form of shared corporate structure. Each party acts independently and on its own behalf. Hannover Re and/or affiliated companies of the Hannover Re Group assume no liability for the accuracy, completeness, or future applicability of the information provided in this document. We consider regulatory obligations in AI solutions for our clients and specifically ensure full compliance with the EU AI Act while maintaining a careful and security‑focused approach to deploying and managing AI systems.