Leveraging electronic health records for smarter, quicker underwriting and claims decisions

This case study highlights how electronic health records enhance underwriting and claims efficiency by providing fast, objective medical information, while also expanding opportunities to offer coverage to insurance applicants.

Loading ...

Background

Traditional underwriting and claims processes often depend on applicants self-reporting on medical history via lengthy forms. When underwriting substandard cases, insurance carriers request supplementary medical reports, which may be difficult for applicants to obtain or to process through an automated underwriting channel. Similarly, some claims rely on medical reports from Medical Doctors or General Practitioners (GPs), which may take lengthy periods of time to obtain and require extensive review and processing before a decision can be made. Electronic health records (EHRs) offer a solution for both underwriting and claims processes, enabling a faster, more streamlined customer journey whilst providing robust, objective medical information that provides insight into the applicant’s health status.

Hannover Life Re of Australasia (HLR Aus) has conducted a range of different pilot programmes to explore EHR integration in underwriting and claims, aiming to improve efficiency and customer experience.

- The first pilot assessed whether patient summaries from PMSs could be mapped to underwriting rules. 60,000 records across three age groups were analysed. All summaries were mappable; over 60% showed no long-term conditions or medications. Of those with conditions, 78% were accurately mapped. Less than 10% of the data was irrelevant. Notably, the top 10 medical risk categories accounted for 80% of EHR health data - a key insight for rule development.

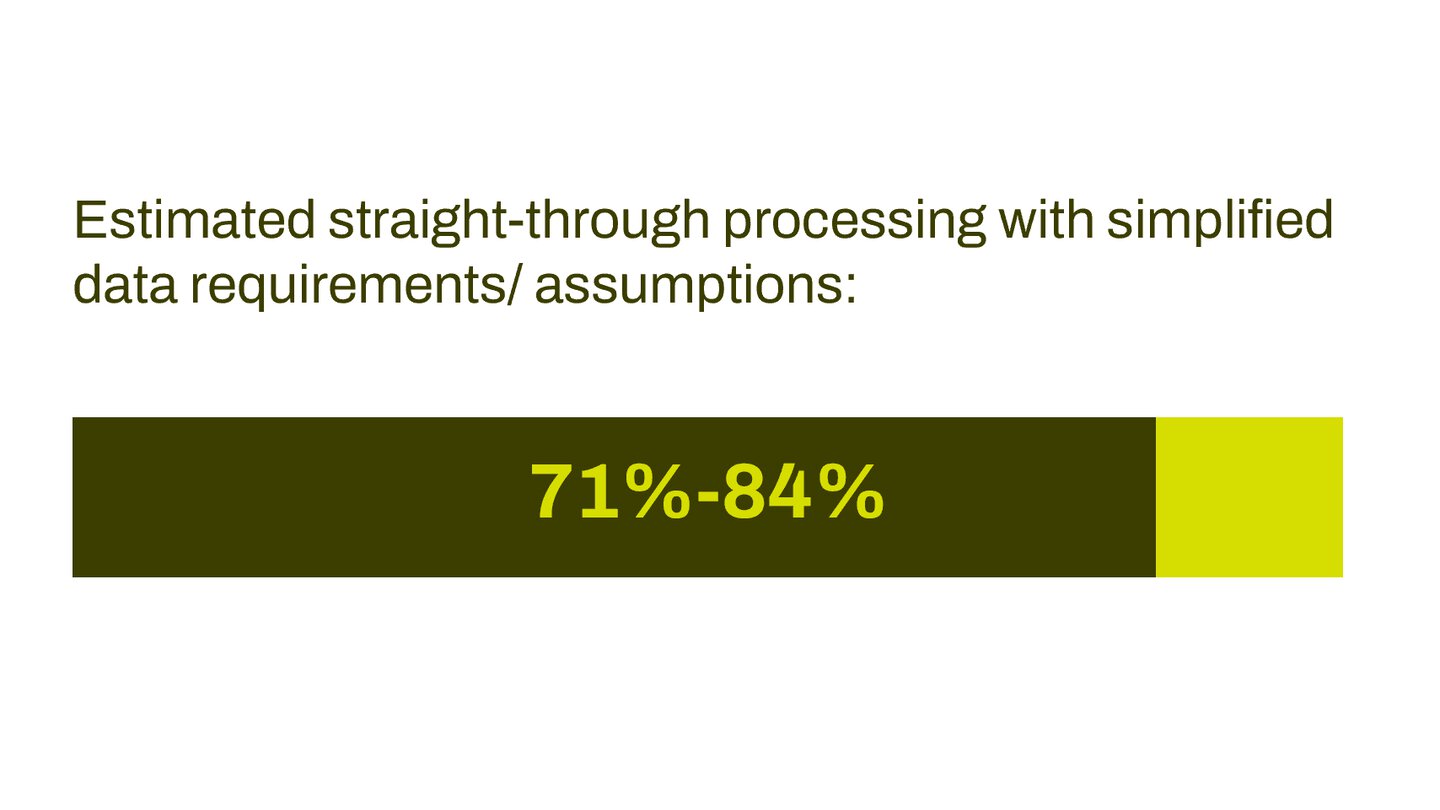

- The second pilot validated these findings using 660 weighted records across 24 subcategories. HLR Aus tested whether patients could be automatically underwritten using health summaries alone and tiered the data by criticality. Completeness was 68% for level 1 (most critical) and 30% for level 2. This suggested that simplifying data requirements or applying assumptions could improve straight-through processing (STP), estimated at 71–84%.

EHRs key pilot results

- The third pilot tested feasibility in a live direct-to-consumer setting, in partnership with a healthcare technology group. Over six months, our healthcare technology partner securely retrieved health data from consenting applicants with ongoing medical conditions. By assessing these records, we demonstrated the potential value of using targeted, verified and structured health data in underwriting. The aim of the pilot was to streamline manual processes and enable automated assessments, and offer cover to applicants previously considered too high-risk.

- The fourth pilot focused on in-flight income protection claims, utilising structured claim form fields that seamlessly integrate with GPs’ practice management systems. This approach reflexively retrieves structured information directly from GPs, streamlining the data collection process. The primary objective was to assess whether the quality of data provided was improved, and to evaluate potential efficiency gains, such as expedited decision making, enhanced triaging, and a reduction in the back-and-forth communications with GPs. Early findings suggest that integrating structured data in this way can accelerate claims handling while maintaining robust and reliable information.

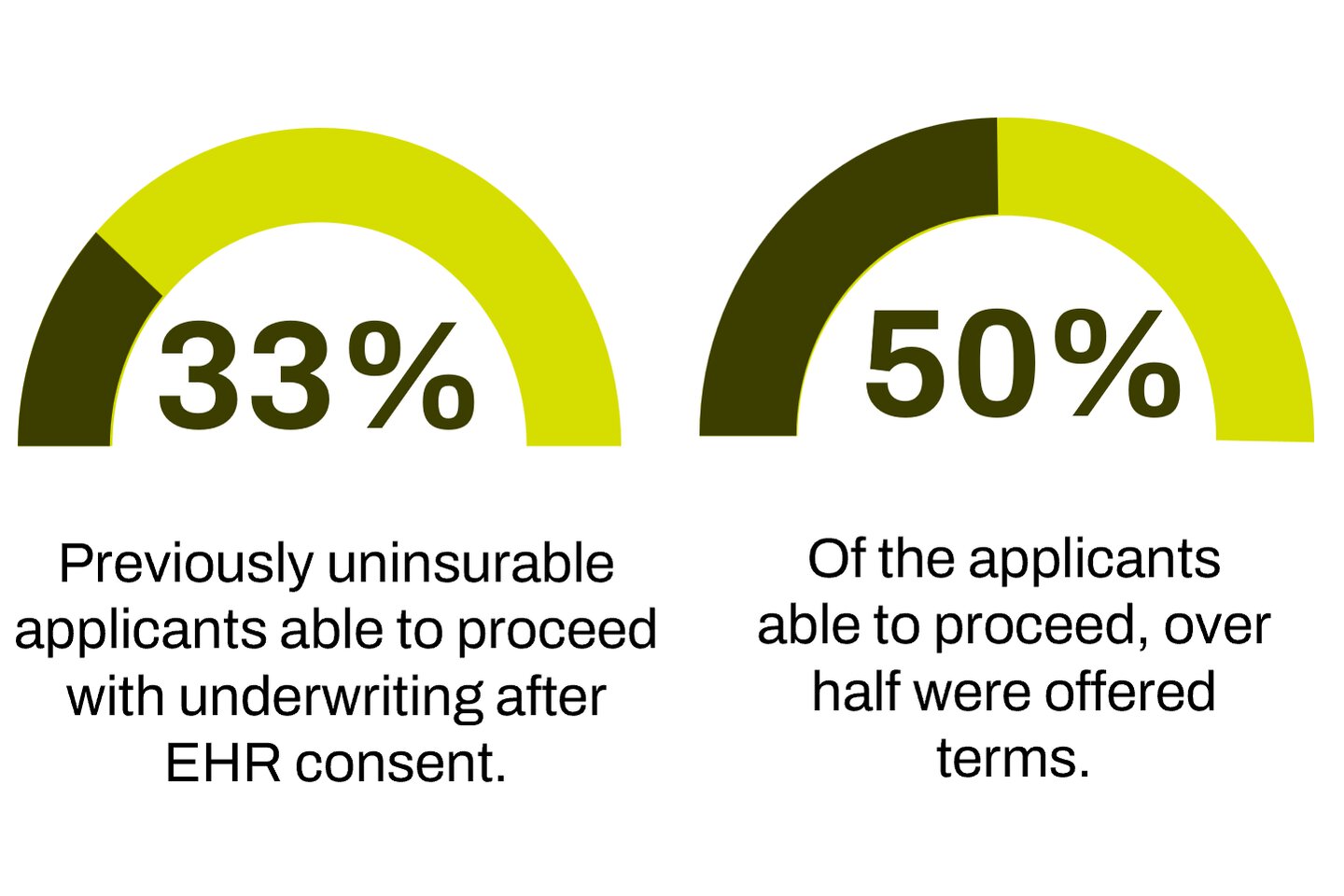

Results of pilot programme

With EHR consent, nearly one third of previously uninsurable applicants could proceed, with over half offered terms.

The pilot confirmed the potential of EHRs while highlighting the need to support GPs with onboarding and improved invoicing practices.

.png)

"Because Electronic Health Records are comprehensive and reliable, they help insurers assess risk fairly and accurately, building customer trust and reducing the need for lengthy questionnaires.

Real-time access to verified health data could enable fully automated underwriting and claims processes, meeting demand for seamless services while improving risk assessment."

Implementation & process considerations

Key lessons from the pilot include:

- The importance of minimising disruption to existing workflows and safeguarding customer trust. Demonstrating that EHR integration is smooth, secure and valuable is essential. Success relied on collaboration across stakeholders, with clear roles, effective communication and accurate documentation.

- To benefit customers, the EHR solution must be reliable and trustworthy. Partnering with reputable vendors is important to achieve GP engagement.

- Robust data governance and compliance are vital to securely manage personal data.

The value of EHRs depends on data quality. Unreliable or incomplete records reduce utility and may trigger unnecessary follow-ups. Starting with targeted use cases with high-quality data tends to deliver the greatest impact and can be scaled over time.

How Hannover Re can support you

EHRs have the potential to transform insurance, from underwriting and claims to customer engagement throughout the policy lifecycle. Real-time access to verified health data could enable fully automated processes, meeting expectations for seamless service and improving risk precision. Hannover Re is keen to further explore the value of EHRs in the following use cases:

- In claims, using EHRs to trigger automatic initiation, ensuring timely support and operational efficiency.

- In policy lifecycle management, authorised access to EHRs when policies are in-force could support prevention-focused models, encouraging healthier lifestyles, early detection and targeted interventions, all without compromising risk pricing.

- In distribution, insurers could expand direct-to-consumer underwriting, waive medical tests when data is available, and simplify products. Enhanced risk precision could improve pricing and broaden customer access.

Together, these developments are shaping a digital, data-driven ecosystem for sustainable underwriting, better customer outcomes, and high-quality automated decision-making.

Reinsurers, insurers, healthcare providers, and technology partners must collaborate to build a future that puts customers first and delivers lasting value across the ecosystem. We welcome the opportunity to discuss - please do get in touch.

Disclaimer:

The information presented in this case study, as well as in any other descriptions of projects or cooperations, is for general informational purposes only and does not constitute legal advice, regulatory guidance, medical advice, or any form of professional advisory service. To avoid any wording that could be interpreted as implying medical effectiveness, this document must not be understood as containing, asserting, or suggesting any medical efficacy claims. Nothing in this document shall be construed as a legally binding offer to enter into any contract or agreement of any kind. All results, performance indicators, and outcome descriptions reflect the specific conditions and parameters of the referenced project(s) or product launch(es). They are not guarantees, promises, or assurances of comparable or future performance in any other context. No warranty is given – whether express or implied – particularly that comparable or similar results can or will be achieved elsewhere. Any potential success of comparable initiatives critically depends on the lawful and compliant ability to contact policyholders, including the validity of any required consent under the applicable legal framework. All third‑party entities mentioned in this document, including insurtech companies, are independent businesses and operate separately and autonomously from Hannover Re. Their services, solutions, or technologies are neither endorsed nor guaranteed by Hannover Re and are subject to their own terms and conditions, unless explicitly stated otherwise. References to third‑party trademarks or brands are made solely for descriptive purposes and remain the property of their respective owners. No affiliation, sponsorship, approval, or endorsement by those owners is implied. Statements in this document regarding benefits, compliance requirements, risks, risk assessments, or business cases are based on our subjective experience, judgment, or interpretation. They do not replace - and must not be relied upon as a substitute for - independent assessment, verification, or due‑diligence activities by customers or other stakeholders. In particular, all aspects relating to data protection requirements (including but not limited to GDPR considerations) and AI‑related regulatory obligations must be independently assessed, verified, and evaluated by interested parties in light of their own legal and operational frameworks. The use of the terms such as “partner” or “partnered” without further qualification solely indicates that we cooperated on specific activities or exchanges with third parties; it does not imply a legal partnership, joint venture, affiliation, or any form of shared corporate structure. Each party acts independently and on its own behalf. Hannover Re and/or affiliated companies of the Hannover Re Group assume no liability for the accuracy, completeness, or future applicability of the information provided in this document.